Member-only story

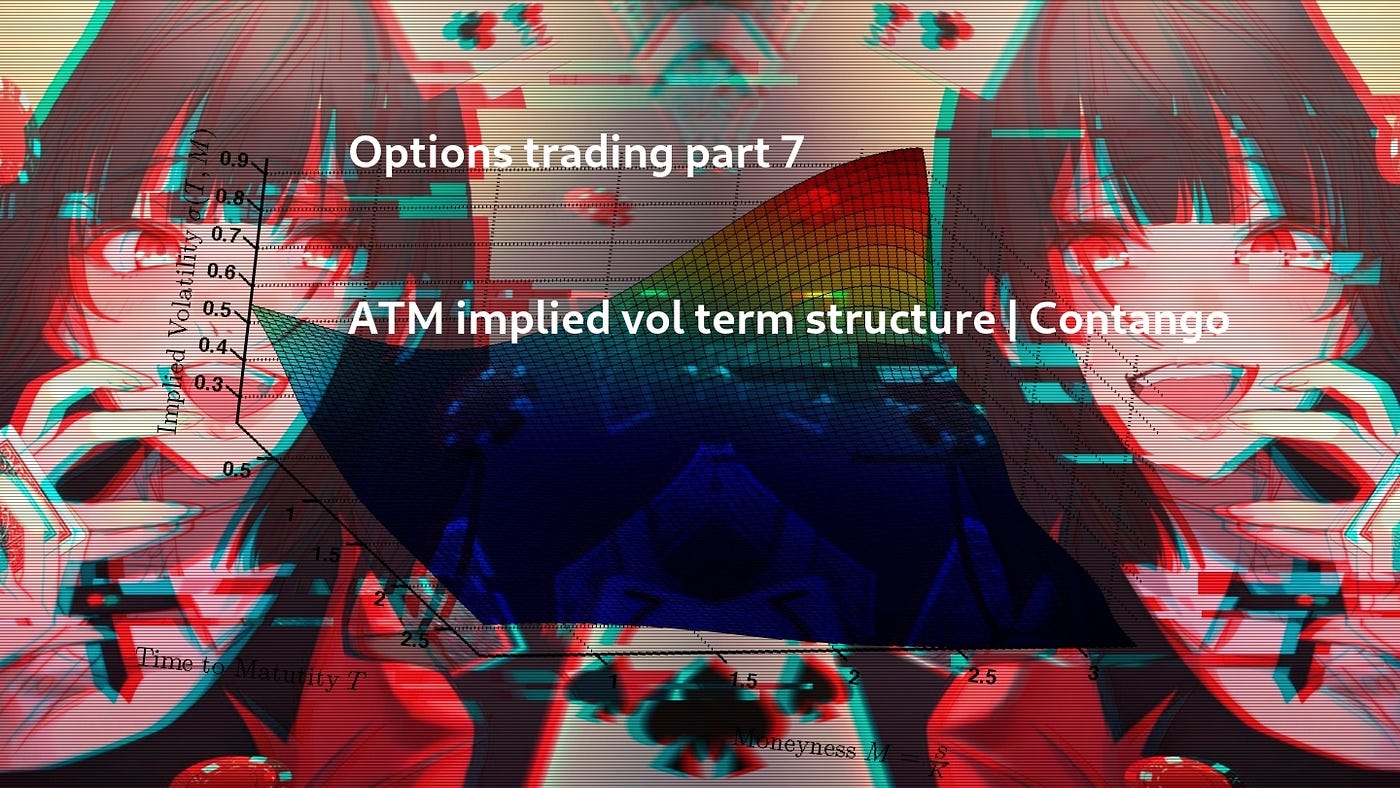

Options trading part 7: ATM implied vol term structure | Contango

The ATM implied vol term structure is a measure we can use to evaluate the “implied volatility” of the options contracts across all the different maturities.

Nonetheless, let’s start with the fundamentals and define what a contango market is.

In a contango market, market participants are more willing to pay a premium for long-term contracts than short-term ones. That is because they anticipate more price increases in the future. In consequence, long-term contracts trade at a premium over short-term contracts.

That type of market condition exists when the demand for a commodity expects to increase in price later. Investors are willing to pay more for a long-term contract because they expect the premium to increase even further.

That often happens when there is an expectation of inflation, as investors want to protect themselves from rising prices.

In the next article, I will try to cover what backwardation is.

Disclaimer:

You have learned in school, on television, or on YouTube how to visualize atoms, protons, neutrons, electrons, etc.

This model is entirely inaccurate, yet we use it because it helps us visualize the specifics of these abstract subjects.

Consider everything in this article to be an oversimplification to assist you with more advanced reading about options trading